How to Write a Check, Step by Step

Key takeaways

- A check has six fields, and getting all six right is what makes it valid and hard to alter.

- Write the amount in words on the legal line and draw a line through any leftover space so no one can add to it.

- The numbers printed along the bottom are your routing number and account number, and anyone who sees them can pull money from your account.

- To void a check, write VOID in large letters across the front, but never throw a blank signed check in the trash.

- Record every check in a register the moment you write it, because a check can clear days or weeks later and quietly overdraw you.

- Checks still matter in 2026 for rent, contractors, official payments, and gifts, but a bank transfer is usually faster and safer.

Maybe a landlord still wants a paper check for the rent. Maybe a contractor does not take cards, or the county clerk needs a check for a permit, or you want to tuck a graduation gift into a card. So you pull out the checkbook that has been sitting in a drawer since the last time you needed it, and you freeze. Which line gets the words? What goes in the little box? What do you write if it is not an even dollar amount? Writing a check is genuinely simple once you have done it, but the fields are unforgiving. One blank, one mismatch, or one careless space can bounce the payment or, worse, let someone change the amount. This guide walks every field, in order, with the small safety habits that keep a check from becoming a problem.

The Six Parts of a Check

Every personal check, no matter which bank issued it, has the same six fields you fill in. Learn these once and you never have to think about it again. There is the date in the upper right corner. There is the payee line, which starts with the words Pay to the order of, where you write who gets the money. There is the small box to the right of the payee line where you write the amount in numbers. There is the long line below the payee, often called the legal line, where you write the amount in words. There is the memo line in the lower left, which is optional. And there is the signature line in the lower right, which is the only field that makes the check actually work.

Get all six right and the check is valid, clear, and difficult to tamper with. Skip the signature and it is worthless paper. Leave a gap on the legal line and you may have handed a stranger room to add a zero. The order below is the order most people fill them in, top to bottom, and it is a good habit because it leaves the signature for last, after you have checked the amounts.

Step 1: Write the Date

In the upper right corner, write the current date. Most people write it as month, day, year, like June 26, 2026, or 06/26/2026. Either format is fine. The date is mostly a record, a marker for when the check was written, and it helps you and the payee track the payment later.

A common question is whether you can postdate a check, meaning write a future date so it cannot be cashed until then. You can write a future date, but it is not a dependable way to stall a payment. Banks can often process a check before the date written on it unless you have given them specific instructions to hold it. So do not write a check today and assume the date alone protects your balance until Friday. The flip side is staleness. A check is generally considered stale after about six months, and banks are not required to honor one older than that, though some still will at their discretion.

Step 2: Fill In the Payee on the Pay to the Order Of Line

On the line that reads Pay to the order of, write the name of the person or business receiving the money. Use the full, correct name. If you are paying a company, write the company name as it appears on the bill, not a nickname. If you are paying a person, their full name is safest. Accuracy here matters because this is who is legally allowed to deposit or cash the check.

Write it clearly and start at the far left of the line so there is no room in front of the name for someone to insert another word. When the name is short, draw a line through the empty space that follows it, running to the end of the line. That small stroke closes the door on anyone adding a second payee or altering the name. If you do not yet know who the payment is going to, do not write a blank check. A check with a signature and no payee is an open invitation to whoever finds it.

Step 3: Write the Amount in Numbers

To the right of the payee line is a small box, usually with a printed dollar sign just before it. Here you write the amount as digits, including the cents. For one hundred dollars and no cents, you write 100.00. For forty-two dollars and fifty cents, you write 42.50. Always include the two decimal places for cents, even when the amount is even, so it reads 100.00 rather than just 100.

Write the numbers tight against the left edge of the box, right up against that dollar sign, with no gap. A space between the dollar sign and the first digit is exactly where a thief could squeeze in another number, turning 100.00 into 4100.00. Keep the digits close together and the box leaves no room for edits. This numeric amount should match the written amount on the next line exactly. If the two ever disagree, the written words are the ones the bank is supposed to honor, so the words are what truly control the payment.

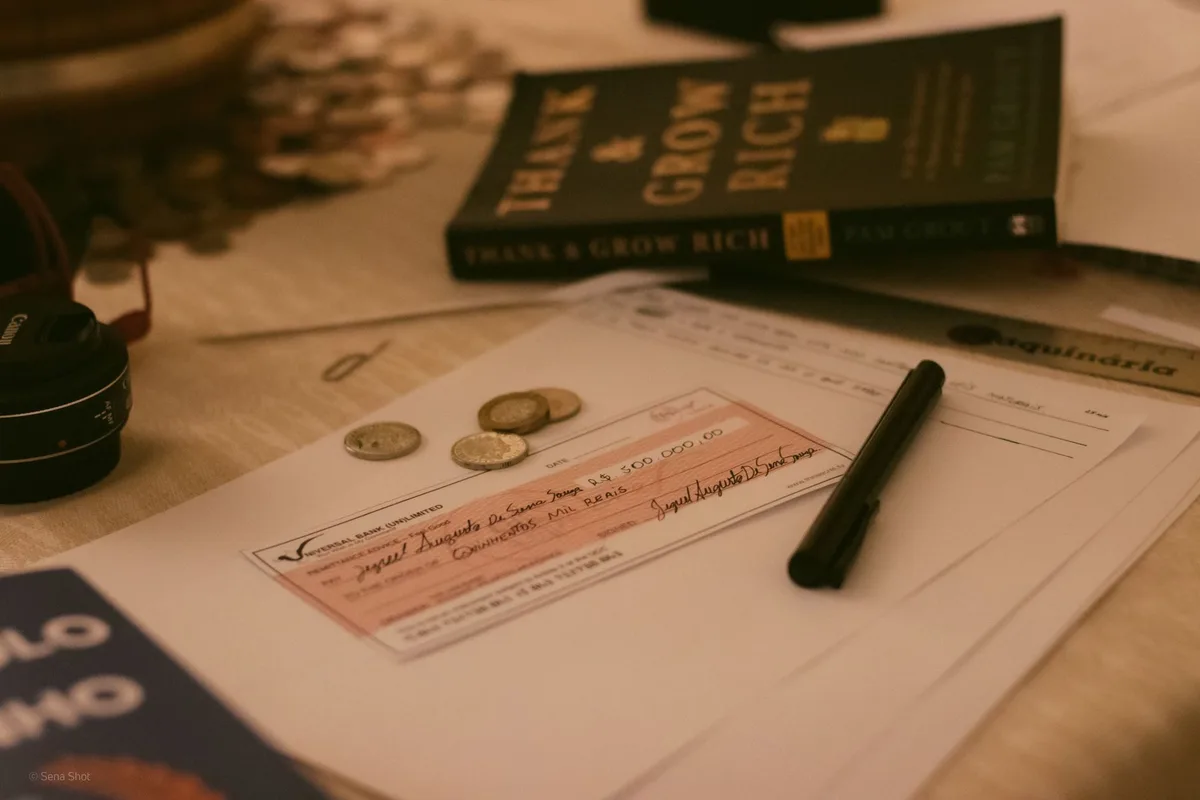

Step 4: Write the Amount in Words on the Legal Line

This is the field that trips people up, so here is the rule clearly. On the long line below the payee, write out the dollar amount in words, then write the cents as a fraction over 100. The word and separates the dollars from the cents, and many people place it where the decimal point would go.

Say you are writing a check for $1,256.75. On the legal line you write: One thousand two hundred fifty-six and 75/100. Notice there is no word and inside the dollar portion. You do not write one thousand two hundred and fifty-six. The only and is the one that stands in for the decimal point, separating dollars from cents. The cents are always written as a fraction of 100, so 75 cents is 75/100, and 5 cents would be 05/100. For an even amount with no cents, say $300.00, you write Three hundred and 00/100, or you can write Three hundred and no/100. Both are accepted.

After the fraction, draw a horizontal line through any remaining blank space all the way to the end of the legal line, or to the word Dollars that is preprinted there. This is the single most important anti-fraud habit on the whole check. That line of ink means no one can add and seventy-five thousand after your amount. The table below shows several amounts written out the correct way, including the awkward small ones.

Step 5: Use the Memo Line

In the lower left corner is the memo line, sometimes labeled For or Memo. This field is optional and does not affect whether the check is valid, but it is genuinely useful. Write what the payment is for, like June rent, or Invoice 4471, or the last four digits of an account you are paying. Billers often ask you to put an account number here so they can match your payment to your account.

One word of caution. Do not write a full account number, a Social Security number, or any sensitive information you would not want a stranger to read. A check passes through many hands and machines, and the memo line is visible to all of them. Keep it to a short, useful reference and nothing more.

Step 6: Sign the Check

The signature line is in the lower right corner, and this is the field that turns a piece of paper into money. Sign it the way your signature appears on file with your bank, using the name the account is held under. An unsigned check is not valid and the bank will not pay it.

Because the signature is what authorizes payment, save it for last. Sign only after you have confirmed the date, the payee, and that the numeric box and the written line agree. Never sign a blank check and never sign one with the amount left open to fill in later. A signed check with blanks is the most dangerous thing in your checkbook, because whoever holds it can complete it however they like. Use a pen with permanent dark ink, not pencil and not erasable ink, so nothing on the check can be rubbed out and rewritten.

How to Write a Check for Cash

Sometimes you want to turn a check into cash at your own bank, or you simply do not have your debit card. You can write a check payable to Cash. On the payee line, instead of a name, you write the single word Cash. Fill in the amount in numbers and words exactly as you normally would, and sign it. Present it to a teller at your bank with your photo identification, and they can hand you the cash if your account covers it.

Understand the risk before you do this. A check made out to Cash is like cash itself. If you lose it or it is stolen before you reach the teller, anyone who holds it can cash it, because no specific payee is named. For that reason many people prefer to write their own name on the payee line instead, which means only they can cash it with their identification. Either way, do not write a check to Cash and carry it around for days. Write it at the bank, or right before you go.

How to Void a Check

Voiding a check means canceling it so it can never be used as a payment. You do this when you make a mistake while writing one, or when an employer or biller asks for a voided check to set up direct deposit or automatic payments. They want the voided check because it shows your routing and account numbers, which they need to link to your account, while the word VOID stops anyone from cashing it.

To void a check, take a pen and write the word VOID in large letters across the front of the check. Make the letters big enough to cover the payee line, the amount box, and the signature line, so the check cannot be filled in or cashed. Do not sign it. Then record it in your check register as void so the check number is accounted for and you are not left wondering later why one is missing. If you only made a small writing error and have not given the check to anyone, the cleanest move is usually to void it and write a fresh one rather than scribbling over the mistake, since a messy check may be rejected.

Never throw an unvoided, signed, or even blank check straight into the trash. A blank check still carries your account and routing numbers, and a thief can use those alone to attempt withdrawals. Shred any check you are discarding.

How to Read a Check: Routing and Account Numbers

Along the very bottom of every check runs a line of stretched-out numbers printed in a special font. These are not decoration. They are the instructions that tell the banking system where the money lives, and you should understand them, because anyone who sees them can attempt to pull money from your account.

There are three groups. The first group, on the far left, is your nine-digit routing number, also called an ABA routing number. It identifies your specific bank. The second group is your account number, which identifies your individual account at that bank. The third group, usually on the right, is the check number, which matches the number printed in the upper right corner of the check. The order can vary slightly by bank, but the routing number is almost always the nine-digit group on the left.

Here is why this matters for safety. Those bottom numbers, your routing and account numbers, are exactly what someone needs to set up an electronic withdrawal from your account. That is why a stolen or photographed check is dangerous well beyond its written amount. It is also why you should be careful about who you hand a check to and never post a photo of one online. The diagram below maps all six fields you fill in plus the three numbers printed at the bottom.

Check Holds and How Long a Check Takes to Clear

When you deposit a check someone gives you, the money does not all become usable instantly, and it is important to understand the difference between funds being available and a check actually clearing. These are two separate events, and confusing them is how people get burned.

Under federal rules, your bank generally must make at least the first $275 of a check deposit available quickly, often by the next business day. The rest typically follows within a couple of business days for most checks, though banks can place longer holds in certain cases, such as a very large check, a new account, or a check that looks suspicious. Availability means you can withdraw or spend that money. It does not yet mean the check is good.

Clearing is the slower, deeper process where the money actually moves out of the check writer's account and settles into yours. A check can be made available to you and still bounce days later if the writer's account did not have the funds or the check was fraudulent. When that happens, the bank pulls the money back out of your account, and you are responsible for it. This is the engine behind countless scams, where someone sends you a check, asks you to send part of the money back right away, and disappears before their bad check bounces. The safe rule is simple. Do not spend or send money against a check until you are certain it has fully cleared, not merely that the funds showed as available.

Keeping a Check Register and Balancing It

A check can clear days or even weeks after you write it, which means your bank balance and your real available money are not the same number. The fix is a check register, the little booklet that comes with your checks, or any simple ledger or spreadsheet. It is the single habit that prevents most overdrafts.

The discipline is to record every transaction the moment it happens. Each entry has a few columns. The check number or transaction type, the date, who it was to or what it was for, the amount, and a running balance. When you write a check, subtract its amount from your balance right then, even though the money has not left yet. When you make a deposit, add it. Do the same for debit card purchases, ATM withdrawals, automatic payments, and fees. The running balance you keep is your true spendable money, because it already accounts for checks that have not cleared.

Balancing, sometimes called reconciling, is when you compare your register against your bank statement or app once a month. You check off every transaction that appears in both. Anything in your register that the bank has not yet processed is an outstanding item, usually a check that has not cleared, and you account for it. If your numbers do not match after that, you hunt for the difference, which is often a forgotten fee, a transaction you did not record, or a simple arithmetic slip. The example register below shows how the running balance protects you from a check you wrote that has not yet hit your account.

Protecting Yourself Against Check Fraud

A paper check is one of the most information-rich documents most people ever hand to a stranger. On one small slip it carries your name, your address, your bank, your routing number, your account number, and your signature. That is why a few defensive habits are worth making automatic.

Use permanent dark ink, never pencil, so your entries cannot be erased and rewritten. Fill every field completely and tightly, with no gaps, and always draw that line through the leftover space on the legal line and after a short payee name. Match the numeric box and the written line exactly. Keep your checkbook somewhere secure, not loose in a bag or car. When you mail a check, drop it inside a post office rather than leaving it in an unsecured outgoing mailbox, because mail theft followed by check washing, where thieves chemically erase the ink and rewrite the check to themselves, is a real and growing problem. Watch for unexpected checks arriving with a request to send money back, which is almost always a scam built on the clearing delay described above. And when you order new checks, track when they arrive, since checks stolen in transit are a known fraud route. If you ever spot a check or withdrawal you did not authorize, report it to your bank immediately, because the speed of your report can affect what you are liable for.

When Checks Still Matter in 2026, and When to Skip Them

Check use has fallen dramatically, but checks have not vanished, and there are still moments when one is the right tool or the only tool. Some landlords and small property managers still prefer or require a paper check for rent. Many contractors, tradespeople, and small vendors take checks when they do not accept cards. Certain official payments, like some government fees, permits, or court-related payments, may ask for a check or money order. And a check tucked in a card remains a traditional way to give a gift, especially across generations.

One of the most common reasons people still mail a paper check is to chip away at a credit card or loan balance, sending the same fixed payment to the lender each month. If that is you, it helps to see how a steady monthly check actually draws the balance down over time, and how much of each payment is eaten by interest along the way. Move the sliders below to set your balance, your interest rate, and the monthly check you mail, and watch how the payoff plays out.

For almost everything else, an electronic option is usually faster and safer. A bank-to-bank transfer or your bank's online bill pay can send money without ever exposing your account numbers on paper. Bill pay services will even print and mail a check on your behalf when a payee does not accept electronic payment, which keeps your own checkbook out of circulation. Person-to-person payment apps handle casual transfers between people you trust. The honest comparison is below. Choose a check when the recipient needs one or when you want a clear paper trail, and reach for an electronic transfer the rest of the time.

A Quick Recap You Can Use at the Counter

If you only remember the shape of it, you will be fine. Date in the corner. Payee on the Pay to the order of line, written to the far left. Amount in numbers in the box, tight against the dollar sign. Amount in words on the legal line, with the cents as a fraction over 100, followed by a line through the empty space. A short note on the memo line if it helps. Your signature last, after you have checked everything else. Then write it in your register before you do anything else, so a future version of you is not surprised when it clears. That is the whole skill. Six fields, a couple of protective strokes of the pen, and a habit of writing it down.

Banks profit from what their customers do not know.

Every fee, teaser rate, and disclosure is a test you are taking whether you study or not. The Financial IQ Test scores your real money knowledge across 90 tests and shows you the gaps before a bank finds them first.

Test your Financial IQQuestions people ask

What do I write if a check is for less than a dollar, like 75 cents?

On the numeric line you write 0.75 or just .75, and on the legal line you write the cents as a fraction of 100. So 75 cents becomes the words zero dollars and 75/100, or simply 75/100 with the word Only afterward. Some people write Only seventy-five cents to be clear. Draw a line through the rest of the legal line so the amount cannot be changed.

Does the date on a check actually matter?

Yes, but maybe not the way you think. The date is mainly a record-keeping marker, and banks can often cash a check before a future date written on it unless you give specific instructions to hold it. Postdating a check is not a reliable way to delay a payment. A check is also considered stale after about six months, and banks are not required to honor one that old, though some still will.

What happens if the numeric amount and the written amount do not match?

The written words on the legal line legally win. Banks are instructed to pay the amount spelled out in words when the two disagree, because words are harder to alter than digits. In practice a mismatch often gets the check flagged or returned, which delays the payment. Always make the box and the line agree exactly so there is no confusion and no delay.

Is it safe to write a check at all in 2026?

It can be, but a paper check exposes more than most people realize. It shows your name, address, bank, routing number, account number, and signature all on one piece of paper. Mailed checks are a known target for theft and check washing. For routine payments, an electronic bank transfer or bill pay is generally safer because it does not put your account numbers in the open. When you must use a check, mail it from inside a post office and use dark permanent ink.

How long does a check take to clear?

Funds availability and full clearing are two different things. Under federal rules your bank usually must make at least the first $275 of a deposited check available quickly, often the next business day, with the rest following within a few business days. A check has not truly cleared until the money has actually moved from the other person's account, which can take longer. A deposit can be made available and still bounce later, so do not spend against a large check until you are certain it has fully cleared.

Can I write a check to myself to move money or get cash?

Yes. To get cash at your own bank, you can write a check payable to Cash or to your own name and present it at the teller window with your ID. Writing a check to Cash is convenient but risky, because a check made out to Cash can be cashed by anyone who holds it if it is lost or stolen. It is safer to write your own name as the payee. To move money between your own banks, many people now use a direct electronic transfer instead.

Keep reading

Never Pay a Bank Fee Again: The Complete Playbook

CD Ladders Explained: Lock In Rates Without Locking Up Your Life

The Emergency Fund Guide: How Much, Where, and How Fast

The Flourish Letter

One useful money idea every Friday, with the interactive chart so you can check the math. Free. Welcome path: free printable toolkit (calendar, debt sheet, raise script, and more).