How to Remove Collections From Your Credit Report

Key takeaways

- You have federal rights the moment a collector contacts you, including a 30-day window to demand written validation of the debt before you pay anything.

- Inaccurate collections can be disputed for free with both the credit bureaus and the furnisher, and unverifiable items must come off your report.

- The statute of limitations on suing you and the seven-year credit-reporting clock are two separate timers, and confusing them can cost you money.

- Pay-for-delete sometimes works but is never guaranteed, so get any deletion promise in writing before you send a single dollar.

- Newer rules removed paid medical collections and any medical debt under 500 dollars, and added a one-year delay before medical debt can be reported at all.

- The most dangerous mistake is re-aging the debt by making a payment or a new promise that restarts the seven-year clock.

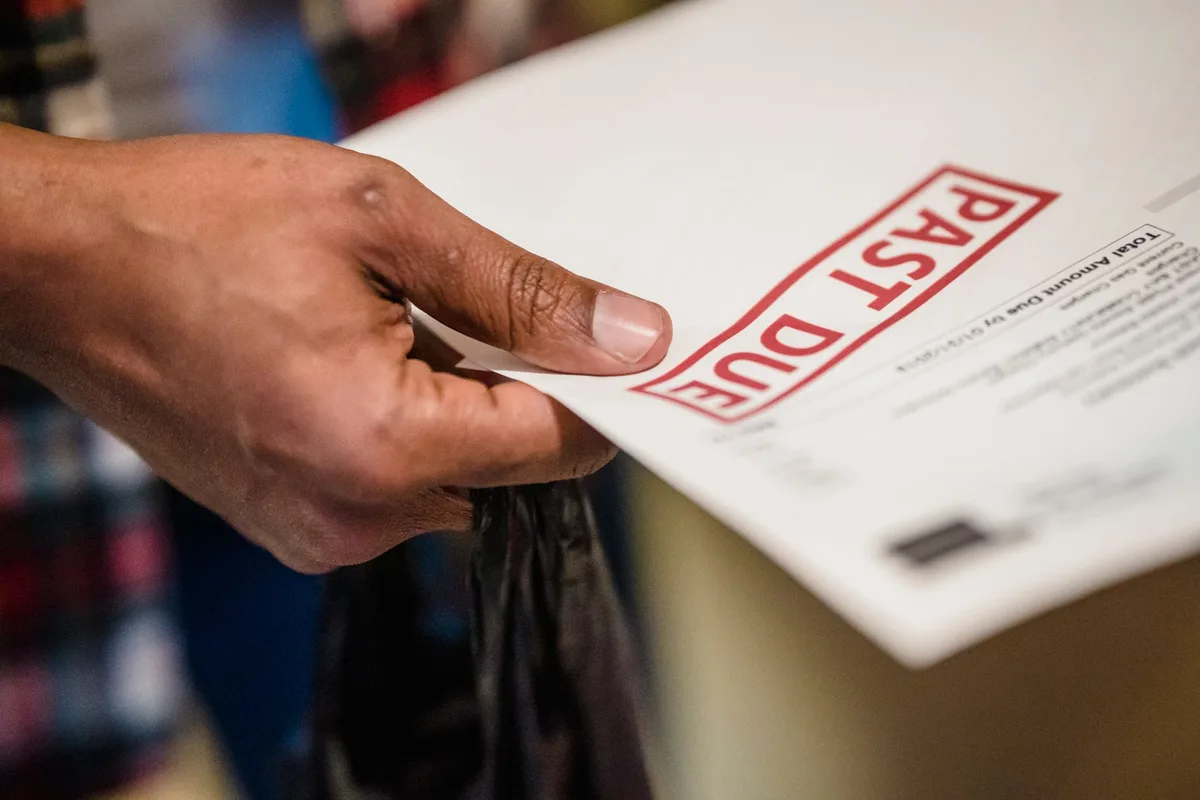

A collection account is one of the loudest negative marks a credit report can carry, and it tends to show up at the worst possible time. You are applying for a mortgage, or a car loan, or a simple apartment lease, and there it is: some balance you half remember, now owned by a company you have never heard of, quietly costing you interest points on everything you borrow. The instinct is to panic and pay it immediately just to make it disappear. That instinct is often wrong, and following it blindly can cost you money and time while leaving the mark right where it was.

This guide walks through the whole process the way a knowledgeable friend would, in order. How the debt got there, how to make the collector prove it, how to dispute what is wrong, and how to think about paying what is real. Along the way we will untangle the two timers that everyone confuses, cover the recent medical-debt rules that erased millions of these accounts, and flag the single mistake that can quietly restart the clock against you. None of this is legal advice. It is a map of the rights and tools that already belong to you under federal law.

How a Debt Ends Up in Collections

Understanding the path matters, because each step leaves a fingerprint you can use later. When you fall behind on a bill, the original creditor usually tries to collect for a few months. Somewhere around 120 to 180 days of nonpayment, that creditor makes a business decision. It can hire a third-party collection agency to chase the debt on its behalf, or it can sell the debt outright to a debt buyer for pennies on the dollar. Either way, a new company now appears on your report as a collection account, separate from the original account.

That handoff creates two important facts. First, the collector may have received sloppy or incomplete records, which is exactly why validation and disputes work as often as they do. Second, the debt now has an anchor date that never moves: the date of first delinquency on the original account. That single date controls when the collection must fall off your report, and no amount of selling, transferring, or re-labeling is supposed to change it. Write that date down if you can find it, because it becomes your most important number.

One more wrinkle. A single old debt can sometimes appear more than once, listed by both the original creditor and the collector, or by two different collectors after a resale. Duplicate reporting of the same debt as two active collections is a common and disputable error, so read your report line by line rather than skimming.

Step One: Pull Your Reports and Read Every Line

Before you contact anyone, get the facts in front of you. You are entitled to free credit reports from all three national bureaus, Equifax, Experian, and TransUnion, and for the last few years those reports have been available weekly at no cost through the official site. Pull all three, because collectors do not always report to every bureau, and a collection can live on one report and not the others.

Now read each report slowly and note, for every collection you find, the following: the collector's name, the original creditor, the reported balance, the account status, and above all the date of first delinquency. Compare that information across the three bureaus, because inconsistencies between them are themselves grounds for a dispute. If Experian shows a delinquency date a year later than TransUnion, one of them is wrong, and the later date is quietly keeping the mark on your report longer than the law allows.

Make a simple list. Which collections look accurate and yours, which look inaccurate or unfamiliar, and which are close to the seven-year mark and may fall off soon on their own. That triage decides everything you do next, because the right move for a legitimate recent debt is very different from the right move for an unverifiable old one.

Step Two: Make Them Prove It With a Validation Letter

The Fair Debt Collection Practices Act, the FDCPA, gives you a powerful tool the moment a collector contacts you. Within five days of that first contact, the collector must send you a written validation notice describing the debt and your rights. And you have 30 days from that first contact to demand validation in writing. When you send a debt validation letter inside that window, the collector must pause all collection activity until it mails you proof of the debt.

That proof should establish that the debt is actually yours, that the amount is correct, and that this particular collector has the legal right to collect it. Send the request by mail and keep a copy, along with proof of mailing. This is not a magic delete button, but it is a genuine filter. Debts that were sold two or three times often come with thin paperwork, and a collector that cannot validate cannot legally keep collecting or continue reporting the item as if it were confirmed.

Even outside the 30-day window you can still ask a collector to verify a debt, and you should if anything looks off. The automatic pause protection is strongest inside the window, but the collector's obligation to report accurate information never expires. If they respond to your request with nothing more than a printout of a balance, that is not real validation, and it strengthens any dispute you file next.

Step Three: Dispute Anything Inaccurate

Here is where the Fair Credit Reporting Act, the FCRA, does the heavy lifting. You have the right to dispute any information on your credit report that is inaccurate, incomplete, or unverifiable, and it costs nothing. There are two places to dispute, and the strongest approach uses both.

First, dispute directly with each credit bureau that shows the error. When you do, the bureau generally has 30 days to investigate. It contacts the furnisher, the collector reporting the item, and asks them to confirm the information. If the furnisher cannot verify it, or simply does not respond in time, the bureau must correct or delete the item. Second, dispute directly with the furnisher itself, because they have their own obligation to investigate and to stop reporting information they cannot back up.

Be specific about what is wrong. A vague dispute that says please remove this gets a weaker response than one that says the date of first delinquency is reported as March 2024 but the account went delinquent in September 2022, or this balance is 400 dollars higher than the original account, or I have no record of ever holding this account. Attach any evidence you have. Filing a dispute never lowers your score, and it is one of the most effective and underused rights you own.

If a dispute succeeds, get an updated report to confirm the item is gone from all three bureaus, not just the one you contacted. If a dispute fails but you still believe you are right, you can add a brief statement of dispute to your file, escalate a complaint to the Consumer Financial Protection Bureau, and in genuine cases of harm, consult an attorney who handles FCRA violations.

The Two Timers Everyone Confuses

This is the most misunderstood part of the entire subject, and getting it straight protects you from expensive mistakes. There are two completely separate clocks, and they have nothing to do with each other.

The first is the credit-reporting clock. Under the FCRA, a collection account can appear on your credit report for seven years from the date of first delinquency on the original debt. After that, it must fall off, whether or not you ever paid it. This clock cannot be restarted by a collector, and it does not reset when the debt is sold. It is about what shows on your report.

The second is the statute of limitations. This is a state law that sets how long a creditor or collector can successfully sue you to collect a debt. It varies widely by state and by type of debt, often somewhere between three and six years, and it is about lawsuits, not credit reporting. Here is the danger. In many states, making a payment on an old debt, or even acknowledging it in writing as yours, can restart the statute of limitations, reviving the collector's ability to sue you on a debt that had become legally unenforceable. A debt past its statute of limitations is often called time-barred.

So the two clocks can point in opposite directions. An old debt might be past the statute of limitations, meaning you cannot be successfully sued, while still sitting on your report for another year or two. Paying it in that situation could restart the lawsuit clock without removing the report entry any faster. Before you pay anything on a very old debt, find out your state's statute of limitations and whether it has already passed.

Pay-for-Delete: The Reality

Pay-for-delete is exactly what it sounds like. You offer to pay a collection, sometimes the full amount and sometimes a negotiated lower settlement, in exchange for the collector agreeing to delete the tradeline from your credit reports entirely, not just mark it paid. When it works, it is the cleanest possible outcome, because deletion beats a paid collection.

The honest truth is that it is inconsistent. Some collectors will do it, especially smaller ones and debt buyers who paid very little for the account. Others refuse, because the agreements they sign with the credit bureaus discourage deleting accurate information, and a collector that deletes verified debts risks its reporting relationship. You will not know until you ask.

Three cautions if you try it. Get everything in writing before you pay a cent, because a verbal deletion promise is nearly worthless and almost impossible to enforce. Make sure the letter names the specific account and says the collector will request deletion from all bureaus that show it. And remember that on an old debt, the act of paying may carry the statute-of-limitations risk described above, so know your state's rules first. Never send money based on a phone promise alone.

Why Medical Collections Are Different Now

Medical debt earned its own set of rules, and those rules erased a huge share of medical collections from consumer reports. If a medical collection is dragging on your report, check these changes first, because the item may not belong there at all.

Three shifts matter most. Paid medical collections are no longer reported, so once a medical collection is paid off, it should come off your report rather than lingering as a paid item for years. Medical collections under 500 dollars are no longer reported at all, which wiped out a large number of small medical accounts. And there is now a waiting period of one year before an unpaid medical debt can appear on your report, giving you time to sort out insurance, billing errors, and payment plans before your credit takes the hit.

Medical billing is famously error-prone, so treat every medical collection with extra suspicion. Verify that insurance was billed correctly, that the amount is right, and that the debt is not something your insurer or a financial-assistance program should have covered. If a medical collection violates any of the newer rules, that is a clean and strong dispute. This is an area where the rules have moved quickly, so confirm the current thresholds when you act.

Goodwill Letters: The Polite Long Shot

If a collection is legitimately yours and you have already paid it, a goodwill letter is worth a try. This is a courteous written request asking the original creditor or collector to remove an accurate but paid negative mark as a gesture of goodwill, usually explaining the circumstances. Maybe a medical crisis, a job loss, or a genuine oversight, followed by a solid record since.

Manage your expectations. Creditors are under no obligation to honor a goodwill request, and many will decline, especially larger ones with rigid policies. It works best when the debt is already paid, the lapse was an isolated event rather than a pattern, and you have been a good customer otherwise. It costs nothing but a stamp and a little humility, so it is a reasonable move once the debt is settled. Just do not count on it as your main strategy, and never pay an unverified debt simply to earn the right to send one.

Paid vs. Unpaid: How the Scores Actually Treat It

Whether paying helps your score depends heavily on which scoring model a lender uses, and this is where a lot of outdated advice leads people astray. Older FICO models, which many lenders still use, count a collection as negative whether it is paid or unpaid. That is the origin of the frustrating truth that paying an old collection sometimes does not move your score at all.

Newer models changed that. FICO 9 and FICO 10, along with the VantageScore 3.0 and 4.0 models, ignore paid collections entirely and weigh unpaid collections more heavily. Under these newer models, paying a collection genuinely helps, because a paid collection stops counting against you. VantageScore models also disregard collections with very small balances. So the same paid collection can be invisible to one lender's model and a live negative to another's, depending on which version they pull.

The practical takeaway is that paying a legitimate collection is more likely to help you than it used to be, especially as newer models spread. But deletion, whether through a successful dispute, a pay-for-delete agreement, or the medical rules, is still the strongest outcome, because it removes the item from every model at once. Paid status helps under newer models. Removal helps under all of them.

The Mistake That Restarts the Clock

We touched on re-aging above, and it deserves its own warning because it is the trap that turns a helpful action into a harmful one. Re-aging happens when the date of first delinquency gets pushed forward, keeping a collection on your report longer than it should stay. Sometimes a collector does this improperly after buying a debt, reporting a fresh date as if the delinquency just happened. That is a reporting violation and a strong dispute, so check that delinquency date carefully against your own records.

The other kind of re-aging is one you can trigger yourself. On the statute-of-limitations side, a partial payment or a written acknowledgment of an old debt can restart the state clock in many places, reopening you to a lawsuit on a debt that had gone time-barred. So before you send money or sign anything on an old account, confirm two things. That your action will not restart the statute of limitations in your state, and that the collector is reporting the correct, original delinquency date. When in doubt on a genuinely old debt, slow down and get advice before you pay.

When to Bring in a Professional

Most of this you can do yourself, and doing it yourself saves money and teaches you the system. But some situations call for a human on your side, and recognizing them is part of being smart with money rather than stubborn.

If you are being sued over a debt, do not ignore it, and strongly consider talking to an attorney, because failing to respond can lead to a default judgment even on a debt you could have challenged. Many areas have legal-aid organizations for people who cannot afford a private lawyer. If a collector is harassing you, calling at odd hours, threatening you, or contacting you after you told them in writing to stop, those are potential FDCPA violations, and an attorney who handles consumer cases may take it at no upfront cost to you. If you are drowning across many accounts and cannot see a path forward, a nonprofit credit counselor can help you build a realistic plan, often on a sliding-fee scale.

Steer clear of credit-repair companies that promise to erase accurate, verifiable debts for a large fee. They cannot legally do anything you cannot do yourself for free, and the ones that promise guaranteed deletion of legitimate accounts are usually selling a fantasy. The Consumer Financial Protection Bureau and the Federal Trade Commission both publish plain-language guidance on every step covered here, and consulting them is free.

Collections feel permanent when you first spot them, but they are not. They are governed by specific rules with specific deadlines, and those rules give you real leverage: the right to demand proof, the right to dispute what is wrong, a hard seven-year limit, and a growing set of protections that already cleared millions of medical accounts. Work the steps in order, protect yourself from restarting the wrong clock, and keep every promise in writing. The mark that looked immovable often turns out to have an expiration date, and sometimes an exit you can open yourself.

The fastest debt payoff plan is usually a bigger shovel.

Every payoff method works better with more income behind it. If your career has plateaued, finding work that matches your cognitive strengths can raise the number that matters most: what you can put toward the balance each month.

Questions people ask

Does paying a collection remove it from my credit report?

Usually not on its own. Paying a collection changes the status to paid, but the account can still appear for the rest of the seven-year reporting period. The exception is medical debt, where paid medical collections are now removed entirely. Payment can still help you with newer credit scores that ignore paid collections.

How long do collections stay on your credit report?

A collection account generally stays for seven years from the date of first delinquency on the original account, not from the date the collector bought it. That original delinquency date is the anchor, and it does not reset when the debt is sold or transferred. After seven years the item must fall off automatically.

What is a debt validation letter and when should I send one?

It is a written request that asks the collector to prove the debt is yours and that they have the right to collect it. Send it within 30 days of their first contact and the collector must pause collection until they respond with validation. Even after 30 days you can still ask, though the automatic pause protection is strongest inside that window.

Is pay-for-delete a legitimate strategy?

It is real but unreliable. Some collectors will agree to delete the tradeline in exchange for payment, while others refuse because their agreements with the bureaus discourage it. Always get the deletion promise in writing before you pay, since a verbal promise is nearly impossible to enforce.

Will disputing a collection hurt my credit score?

No. Filing a dispute does not lower your score, and it is a protected right under federal law. While an item is under dispute it may be flagged, but the dispute itself carries no penalty. If the collector cannot verify the debt, the item must be removed.

Can a collector restart the seven-year clock by contacting me?

No. The seven-year credit-reporting clock is tied to the original date of first delinquency and cannot legally be restarted by a collector. Be careful, though, because a partial payment or a new written promise can restart the separate statute of limitations on lawsuits in many states.

Keep reading

How to Win at Credit Card Rewards Without the Debt Trap

The 800 Credit Score Playbook: What Actually Moves the Needle

Debt Snowball vs Avalanche: The Interactive Showdown

The Flourish Letter

One useful money idea every Friday, with the interactive chart so you can check the math. Free. Welcome path: free printable toolkit (calendar, debt sheet, raise script, and more).